A new report from S&P Global Market Intelligence reveals striking contrasts in the insurance industry’s 2025 performance.

Several property and casualty lines posted historically low loss ratios, while others surged to record highs. The sharp divide paints a dramatic picture of a market experiencing both remarkable profitability and mounting pressure—an eye-opening snapshot that shows just how uneven the year turned out to be across different lines of business.

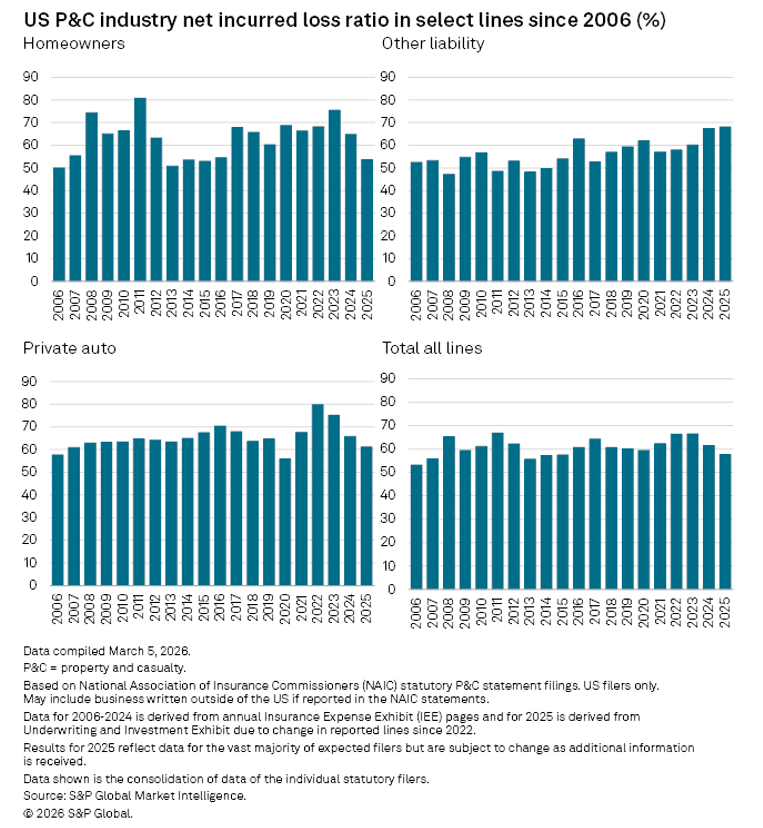

Unsurprisingly, the strongest results emerged in commercial liability lines, where insurers posted some of the highest loss ratios on record. At the other end of the spectrum were personal lines—particularly homeowners insurance, which is often vulnerable to wildfire risk. That segment saw notably lower loss ratios, helped in part by a rare bit of luck: the United States avoided any landfalling hurricanes last year, giving insurers a much-needed break from major catastrophe losses.

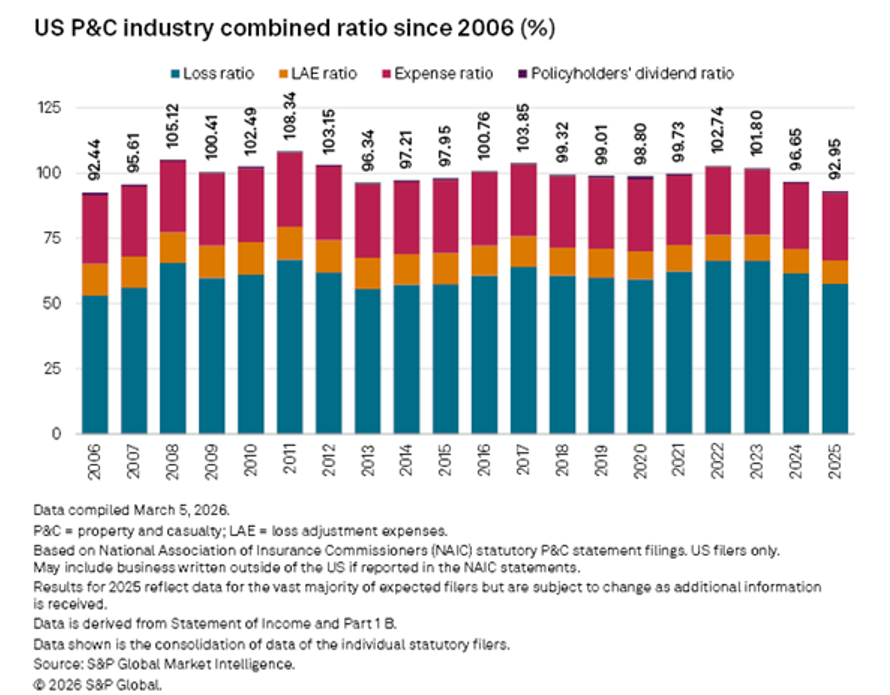

Ultimately, the lows outweighed the highs, according to a report on property/casualty insurers’ statutory financial results from S&P Global Market Intelligence titled “Spectacular P&C Statutory Profitability May Prove Fleeting.” Yet the most important takeaway from last year’s record-setting performance wasn’t simply the divide between personal and commercial lines. Instead, researchers say the real story was the widening gap between property and casualty—two sides of the industry that moved in sharply different directions as 2025 unfolded.

"We can say with conviction that the industry will not replicate these results in 2026, or, quite possibly, at any point in the foreseeable future," wrote analysts Jason Woleben, Tim Zawacki, and Husain Rupawala of S&P Global Market Intelligence in a report released Monday. They noted that 2025 delivered the strongest underwriting performance in 19 years, fueled by a rare alignment of favorable market cycles, lighter catastrophe losses, and aggressive profitability initiatives across the industry. But the momentum may be short-lived. Slowing premium growth and intensifying competition are already casting doubt on whether insurers can come close to repeating such standout results anytime soon.

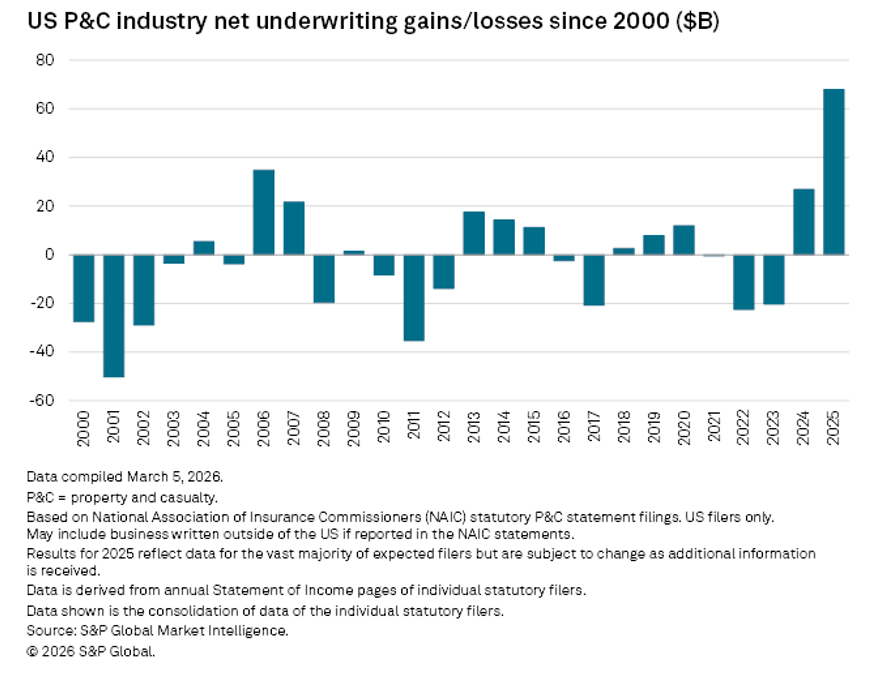

In dollar terms, the property/casualty industry posted a staggering $67.9 billion in net underwriting gains in 2025—easily eclipsing the inflation-adjusted record of $54.2 billion set in 2006. The milestone highlights just how extraordinary the year was for insurers, marking one of the most profitable underwriting performances the industry has ever seen.

The industry’s combined ratio came in just under 93.0—an exceptionally strong result that has been topped only once in the past two decades. The only better performance was a 92.4 combined ratio recorded back in 2006, underscoring just how rare and remarkable the industry’s underwriting strength was in 2025.

When it comes to the biggest winners and losers by line of business, S&P Global Market Intelligence highlighted several striking extremes. The firm’s research on 2025 net loss ratios reveals just how dramatically performance varied across the property/casualty landscape—setting the stage for some eye-opening highs and lows across the industry.

- The homeowners line posted a net loss ratio of 53.7 in 2025—an impressive 11.1-point improvement from 2024 and its strongest performance in a decade. It marked the lowest level since 2015, highlighting just how dramatically conditions improved for insurers in this catastrophe-sensitive segment.

- The private passenger auto segment also delivered a notable turnaround. Its net loss ratio fell to 61.1 in 2025—an improvement of 4.7 points from 2024 and the line’s best result since 2020. Even more striking, the personal auto physical damage segment recorded a net loss ratio of just 52.2, the lowest level seen in at least three decades, underscoring a dramatic rebound in profitability for auto insurers.

- Meanwhile, casualty lines moved in the opposite direction. According to an aggregate analysis by S&P Global Market Intelligence, the net loss ratio for casualty business climbed to 66.7 in 2025. Within that group, pressure was especially evident in several key segments: the loss ratio for other liability coverage surged to a 21-year high of 68.0, while medical professional liability also reached its highest level in more than two decades at 57.9—signaling mounting claims costs across parts of the casualty market.

Notably, private passenger auto liability told a more nuanced story. The subline posted a net loss ratio of 67.9 in 2025—down 2.1 points from 2024 but far from a record. In fact, according to S&P Global Market Intelligence, the personal auto liability loss ratio has been lower than 67.9 in 20 of the past 30 years. The figure reinforces analysts’ broader takeaway: the real dividing line in 2025 wasn’t personal versus commercial business, but property versus liability—an imbalance that ultimately shaped the year’s overall property/casualty underwriting results.

“[E]ven as underwriting results on a total-filed basis improved to levels we may only see once or twice in our lifetimes, several commercial casualty lines showed noteworthy deterioration,” the S&P GMI analysts wrote.

“In addition to the unique confluence of circumstances that led to 2025’s outsized profitability, written premium growth is significantly lagging earned premium growth at respective rates of 4.9% and 6.3% as heightened competition returns to the private auto market and the scourge of social inflation is not going away,” they wrote, further explaining why the industry’s success in 2025 is unlikely to be replicated in 2026.