Commercial property and casualty premiums across accounts of every size hit their lowest point since 2017 in the fourth quarter of 2025, according to the latest quarterly survey from The Council of Insurance Agents & Brokers (CIAB).

The numbers signal a notable shift in market momentum—one that’s turning heads across the industry and raising new questions about where pricing trends may head next.

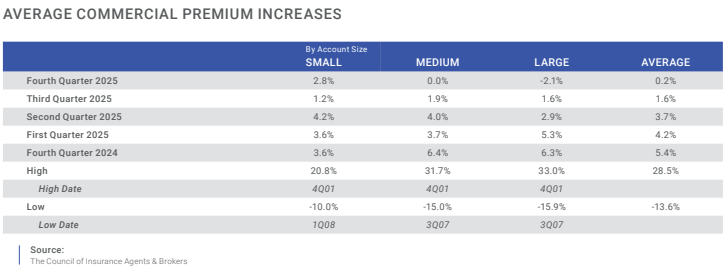

Overall, premiums across accounts of every size edged up just 0.2%—a sharp slowdown from the 1.6% increase recorded in Q3 2025, when CIAB pointed to “clear soft market conditions.” The latest figures suggest the market isn’t just softening—it’s losing steam, setting the stage for what could be an even more competitive pricing environment ahead.

In its latest survey report, CIAB noted that “signs of softened market conditions were equally evident across lines of business.” In other words, the easing wasn’t isolated—it was broad-based, rippling through the market and reinforcing the sense that pricing pressure is steadily giving way to a more competitive landscape.

Nine lines of business—cyber, business interruption, commercial property, construction, directors and officers (D&O), employment practices, surety bonds, terrorism, and workers’ compensation—posted premium declines this quarter, up from six in Q3 2025. Leading the slide was D&O, which fell 3.8%, marking its eighth consecutive quarterly decrease—the longest sustained drop among all major lines and a clear signal that competitive pressures are intensifying.

Even commercial auto—the only line still posting the steepest gains—showed signs of cooling. Premiums rose an average of 6.6%, extending an extraordinary streak of 58 consecutive quarters of increases, but that was down from a 7.4% jump in Q3 2025.

Survey respondents continued to point to social inflation and so-called “nuclear verdicts” as key cost drivers, with roughly half also reporting a rise in claims activity. At the same time, many noted tightening capacity for commercial auto risks—a combination that suggests the line remains under pressure, even as the pace of rate hikes begins to ease.

The average premium increase across all lines of business slowed to 1.9% in Q4 2025—a 30% drop from 2.7% in Q3—according to The Council of Insurance Agents & Brokers (CIAB). Notably, for the first time since Q4 2017, large account premiums actually declined, falling an average of 2.1%.

Survey respondents pointed to intensifying competition for upper-middle-market and large accounts, a shift that suggests carriers are sharpening their pencils and battling more aggressively for high-value business.

According to CIAB, 2017 marked the close of the last soft market cycle captured in its quarterly survey—making today’s pricing trends feel less like a blip and more like a potential turning point in the market’s broader rhythm.