State Farm posted a remarkable comeback in 2025, delivering a $1.5 billion underwriting gain across its property and casualty operations.

That marks a dramatic reversal from a staggering underwriting loss of more than $6 billion in 2024—and follows two consecutive years in which losses topped $10 billion annually. The sharp turnaround signals a powerful shift in momentum, underscoring just how quickly the insurer has moved to stabilize performance and restore profitability.

While the broader return to profitability led State Farm to announce a $5 billion dividend payout to policyholders, the insurer’s core homeowners business is still bleeding red ink. Despite the headline-grabbing rebound, underwriting losses in homeowners coverage continue to weigh on results—an important reminder that not every line of business has turned the corner just yet.

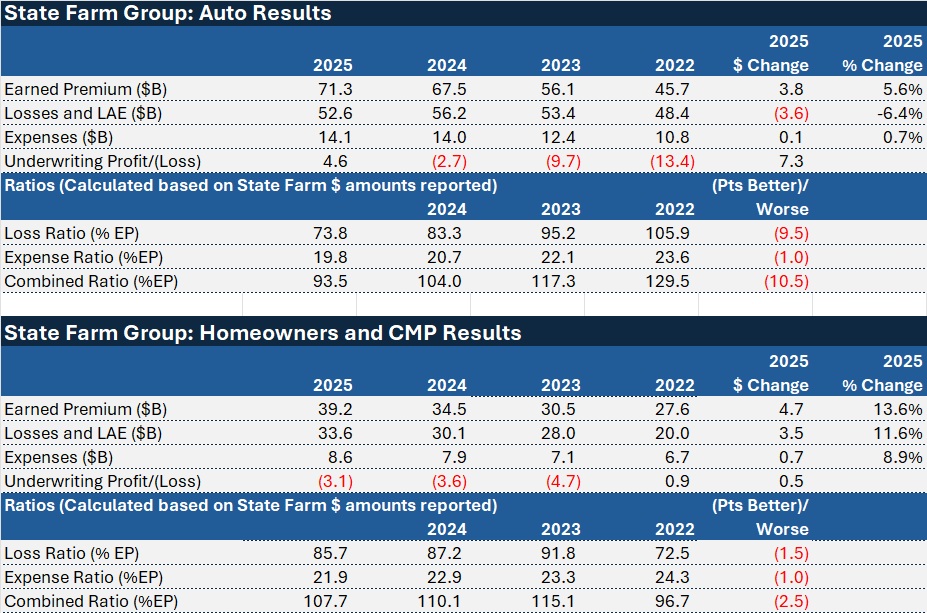

State Farm’s auto business was the engine behind the company’s dramatic turnaround. Auto earned premiums climbed nearly 6% to $71.3 billion, fueling an underwriting profit that came close to $5 billion. The official figure—$4.6 billion—reflects a strong 93.5 combined ratio, an improvement of more than 10 points from 2024’s roughly 104. The sharp swing highlights just how decisively the insurer tightened performance in its largest line of business.

Property told a very different story. Even after earned premiums for homeowners and commercial multiple peril policies surged more than 13% for the second straight year, State Farm’s property combined ratio hovered near 108—just 2.5 points better than in 2024. In other words, stronger pricing and premium growth weren’t enough to fully offset persistent claims pressure, leaving the property line still struggling to break into the black.

State Farm’s statement on its 2025 financial results puts a spotlight on one major driver behind last year’s homeowners underwriting performance: the devastating January 2025 Los Angeles wildfires. The company made clear that the catastrophe left a significant mark on its bottom line, underscoring how a single, large-scale event can reshape an entire year’s results.

"More than 1,000 State Farm employees, agents and agent team members deployed to California to help more than 13,500 customers with claims following devastating wildfires in January 2025." State Farm said in its statement. "To date, State Farm Mutual and State Farm General Insurance Company together have issued over $5 billion in payments to families whose cars, homes and property were damaged or destroyed by those fires."

The insurer added that total payouts could climb to $7 billion as outstanding claims are settled and ongoing repairs and rebuilding efforts are completed—underscoring the full financial weight of the catastrophe.

“Hundreds of State Farm team members remain on the ground in the Los Angeles area assisting customers,” the statement said.

Nationwide, State Farm Mutual Automobile Insurance Company and its property/casualty affiliates reported $78 billion in incurred claims in 2025, including nearly $15 billion tied to catastrophe losses, according to the company’s statement.

When factoring in loss adjustment expenses, total incurred losses climbed to more than $86 billion, based on the separately disclosed auto and property figures in the report. The scale of those numbers underscores the immense claims burden the insurer absorbed over the year—even as it worked to restore profitability.

In all, State Farm said its property and casualty companies generated a combined underwriting profit of $1.5 billion on $111.6 billion in earned premium.

That underwriting gain—paired with $7.0 billion in investment and other income—pushed P/C pre-tax operating profit to $8.5 billion in 2025. The swing is striking: just a year earlier, the insurer posted a $111 million operating loss, following back-to-back annual operating losses of more than $8 billion. The sharp reversal underscores how dramatically the company’s financial trajectory has shifted in a short span of time.

State Farm reported total revenue of $132.3 billion in 2025—including premium income, earned investment income, and realized capital gains and losses—up 7.5% from $123.0 billion a year earlier. The solid year-over-year growth highlights the insurer’s renewed momentum, adding another layer to its broader financial turnaround.

On the bottom line, State Farm delivered net income of $12.9 billion in 2025—more than double the $5.3 billion it earned in 2024. The 2025 figure includes $2.0 billion in realized capital gains, net of tax, giving results an additional boost. Even so, the dramatic year-over-year surge underscores just how sharply the insurer’s earnings power rebounded.

At year-end 2025, State Farm Mutual Automobile Insurance Company reported net worth of $170 billion, up from $145.2 billion at the close of 2024. The sizable increase was driven largely by strong operating profits from its property and casualty affiliates, along with rising values in the P/C companies’ unaffiliated equity portfolios. The jump in surplus further strengthens the insurer’s financial cushion, reinforcing its capacity to weather future volatility while continuing to reward policyholders.

“Although financial information is presented on a group/line of business basis, State Farm Mutual Automobile Insurance Company and each of its affiliates must meet solvency and regulatory requirements on an individual entity-by-entity basis without regard to the solvency or financial condition of any other affiliated entity,” a footnote to the report says.

This footnote isn’t new—it has appeared at the bottom of State Farm’s financial reports for years. But it took on added weight last year as company leaders pushed for homeowners rate increases in California, pointing to the fragile financial position of an affiliated entity—State Farm General Insurance Company, its California homeowners carrier—to bolster the case for regulatory approval. In that context, what once looked like routine fine print became a critical piece of the broader pricing debate.

Beyond P/C

The State Farm group’s insurance operations span 14 property and casualty companies and two life insurance companies—an expansive structure that underscores the scale and complexity behind one of the nation’s largest insurers.

Beyond the $5 billion returned to auto policyholders, State Farm Life Insurance Company and State Farm Life and Accident Assurance Company reported a combined $924 million in dividends to eligible life policyholders—the largest payout in their history, according to State Farm’s media statement. The record-setting distribution underscores the breadth of the insurer’s financial rebound, extending well beyond its core auto business.

State Farm Life Insurance Company and State Farm Life and Accident Assurance Company generated $6.9 billion in premium income in 2025 and posted net income of $2.1 billion. By year-end, the two carriers had $1.2 trillion in individual life insurance in force—an enormous footprint that highlights their scale and enduring presence in the U.S. life market.

State Farm Mutual Automobile Insurance Company also disclosed an underwriting loss of $189 million in its individual health insurance business, written on $756 million in net premiums. While small compared with the group’s broader P/C and life results, the loss shows that not every segment shared equally in the company’s wider earnings rebound.

State Farm’s Investment Planning Services division posted a net loss of $39 million in 2025, even as assets under management totaled $17.5 billion. The contrast highlights a mixed performance within the broader organization—strong asset scale, but profitability that still has room to improve.

Auto Improvement vs. Competitors

Emphasizing the strong turnaround in its auto business, State Farm Mutual Automobile Insurance Company said the one-time $5 billion cash-back dividend for eligible auto customers came on top of meaningful rate reductions. Those cuts delivered roughly $4.6 billion in lower annual premiums for drivers across 40 states—stacking immediate cash in customers’ pockets with longer-term savings and underscoring the scale of the company’s auto recovery.

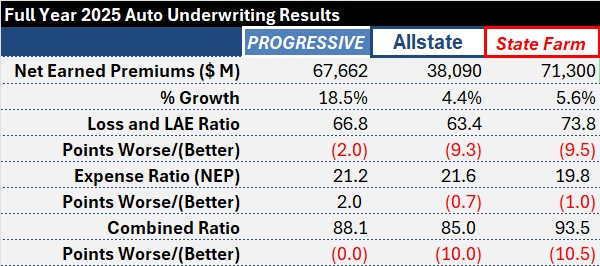

The rebound in State Farm’s property and casualty operations—marked by a nearly 10-point decline in its loss and loss adjustment expense ratio—matched the improvement posted by Allstate and far outpaced the roughly two-point gain reported by Progressive Corporation. The side-by-side comparison underscores just how significant State Farm’s turnaround was in a fiercely competitive market.

All three carriers posted stronger underwriting performance, but State Farm still trails its closest rivals on a key metric. Its personal auto loss and loss adjustment expense ratio came in at 73.8—well above the mid-60s ratios reported by Progressive Corporation and Allstate. The gap suggests that while State Farm’s turnaround is real, there’s still ground to make up in closing the profitability divide.

According to data compiled by Carrier Management from the three companies’ financial reports, State Farm and Allstate lagged Progressive Corporation in auto premium growth in 2025. Progressive’s auto earned premiums surged nearly 19%—more than three times the 5.6% increase posted by State Farm. The stark contrast highlights a widening growth gap, even as underwriting results improved across the board.