We recommend 9 independent contractor insurance companies: CoverWallet, Simply Business, Hiscox, Contractor’s Edge Insurance Services, Zurich, Nationwide, Next Insurance, the Hartford, and Liberty Mutual

There are actually many different types of jobs that fall under the heading of “independent contractor”. An independent contractor could actually be anything—a freelance writer, data entry specialist, computer consultant, tax accountant, or a writer, etc. They all need some sort of independent contractor insurance.

The pandemic caused many formerly employed people to strike out on their own and either start their own businesses or enter the gig economy as freelancers. One of the many questions you may have is what kind of insurance you need. Are you an independent contractor? Do you need liability insurance? Here’s what you need to know.

If you’re confused about what kinds of insurance you might need as an independent contractor, CoverWallet offers a free insurance a-sessment so you can make sure your business is covered. While an independent contractor who does construction work might need general liability, builders’ risk, workers compensation, E&O and professional liability insurance, a freelance writer might just need E&O insurance.

Simply Business is an insurance aggregator, culling quotes from different insurance companies so that you can compare. They work with 10 different companies, including Hiscox and Markel. They can also cover you no matter what sort of independent contractor you are, from photographers to construction workers to IT consultants.

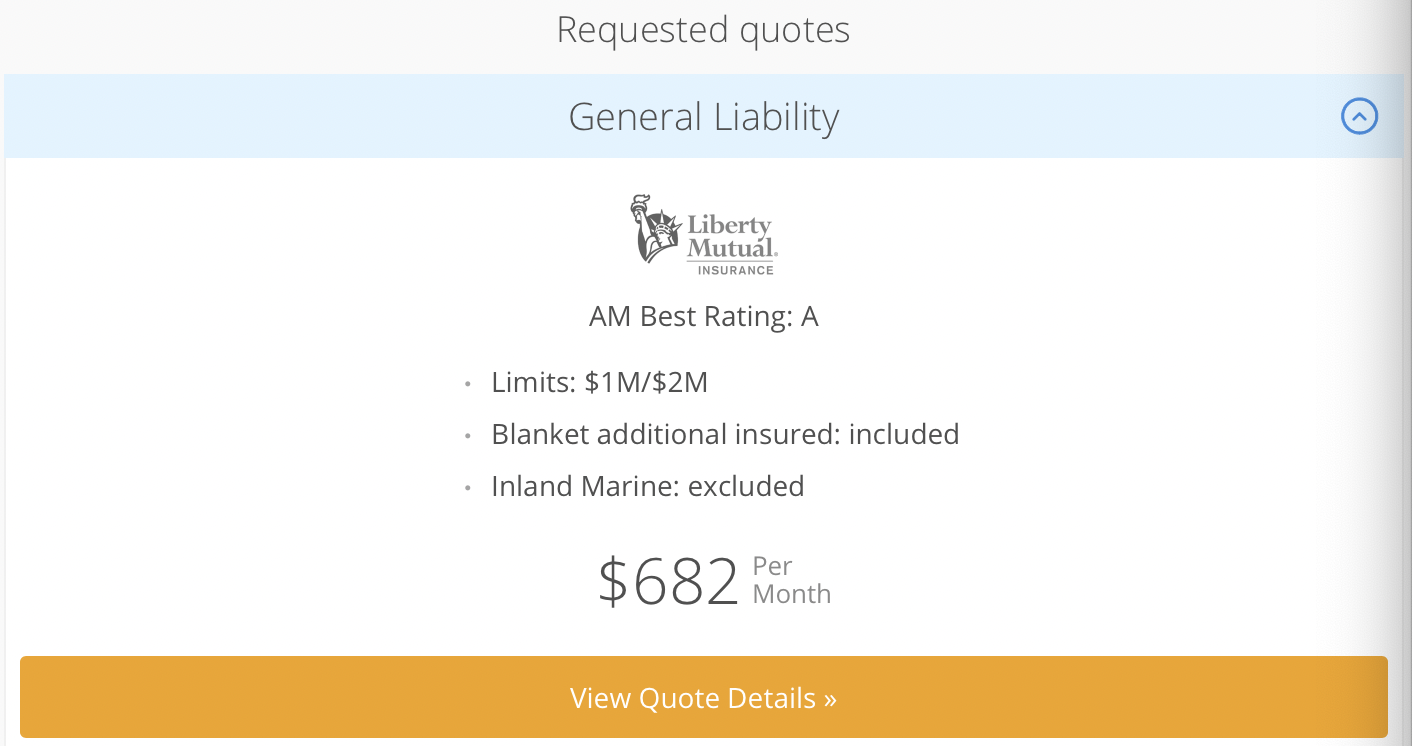

It’s easy to get a quote from Hiscox. When you enter your profession from the drop-down menu, they recommend business insurance you might need. For example, for a computer consultant in Connecticut, it recommended professional liability insurance, and then either general liability or a business owners policy.

/GettyImages-918377524-d6de9dae390340019ed43fdf2392d68d.jpg)

/shutterstock_236845816-5bfc3baa46e0fb00260f517d.jpg)

Former President Joe Biden sparked headlines Friday afternoon after stumbling over the word ‘America’ during remarks criticizing the Trump administration at an LGBTQ rights forum in Washington, DC.

Former President Joe Biden sparked headlines Friday afternoon after stumbling over the word ‘America’ during remarks criticizing the Trump administration at an LGBTQ rights forum in Washington, DC.