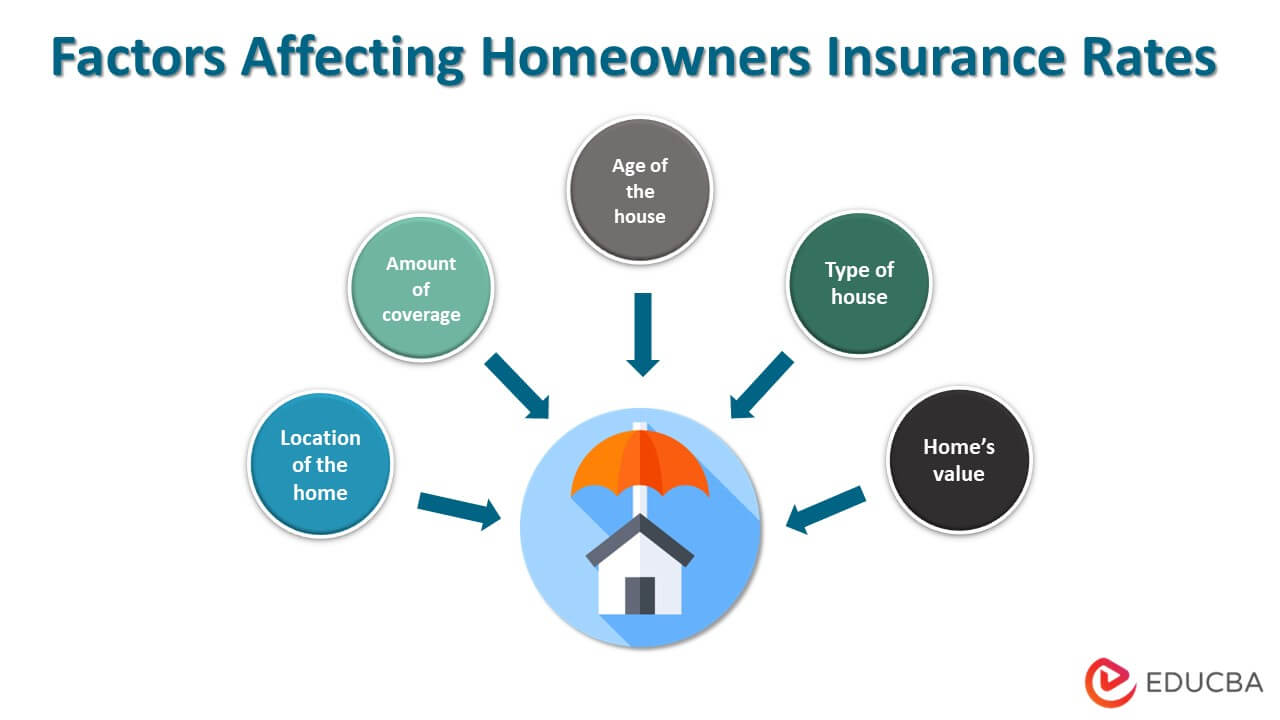

Homeowners insurance is a policy that covers the costs for the loss of a person’s house or damage to the property and its possessions.

Homeowners insurance safeguards the insured property and compensates for any damage/loss to the home and its belongings. For example, Mr. Dawson inherits his family home and decides to buy insurance for the house. He, therefore, purchases $3,000,000 in home insurance. A sudden fire due to an electrical short circuit causes significant damage to the house and its possessions. Mr. Dawson claims the insurance and gets $2,000,000 (the home’s current market value).

Homeowners insurance covers damages from lightning, fire, natural disasters, and more. It generally reimburses for the home and its contents, such as furniture and appliances, and provides liability coverage if someone gets injured on the property.

Some policies also cover temporary living expenses if the residence is uninhabitable. Suppose a home gets damaged in a fire, then the policy may cover the cost of staying in a hotel during repairs on the house

Type

Perils

Coverage

HO-1: Basic

It is the most basic policy that covers limited perils, like fire, theft, vandalism, etc

It pays in actual cash value

HO-2: Broad

It is an advanced HO-1 policy that covers extra perils such as water overflow, freezing, sudden accidental cracking, and more

It compensates for dwelling in replacement costs and property in actual costs

HO-3: Special

It is the most commonly available insurance that provides coverage for most of the perils, excluding earthquakes, sinkholes, etc

It pays replacement costs for both dwelling and property but still can differ on the policy

HO-4: Contents Broad

It is for renters to secure their belongings under most kinds of perils; similar to HO-3

It covers the renters’ damaged possessions in replacement costs. In addition, it can provide living expenses

HO-5: Comprehensive

It covers single-family homes under all possible perils, from fire to snow blockage and more

It covers the damages in replacement costs for all possessions along with the house

HO-6: Unit-owners

It is for people living in condos, and the perils included vary on the plan. It can be limited, or all perils

The coverage is mainly for renovations, liability, a-set losses, etc

HO-7: Mobile Home

It is generally for mobile houses like trailers, modular homes, and others. The perils depending on the plan

It covers the policyholder only for losses when the home is not in transit

HO-8: Modified Coverage

It is an HO-1 policy for houses that do not fall under any other category, such as high-risk location-based homes.

The coverage is for actual cost value, similar to HO-1.

In August 2022, Mark Orminski experienced a fire at his house due to a faulty LED bulb. He claimed the homeowners insurance from State Farm Insurance, and the company had to pay $246,000. However, the company then sued Amazon, where Mark bought the bulb from, as they had warranted it.

:max_bytes(150000):strip_icc()/homedisaster_AP110828045473-5425d4abb8604e1699a29b76123baf65.jpg)

:max_bytes(150000):strip_icc()/HomeownersInsuranceGuide-ABeginnersOverviewcopy-c1c90ab00c1a429a9270e0168fbc9b19.jpg)

Federal authorities have arrested Zhan Petrosyants, accusing him of running a massive no-fault auto insurance fraud ring that funneled tens of millions of dollars through fake medical claims and money laundering.

Federal authorities have arrested Zhan Petrosyants, accusing him of running a massive no-fault auto insurance fraud ring that funneled tens of millions of dollars through fake medical claims and money laundering.