Find out how much of a health insurance subsidy you can qualify for.

Health insurance is often expensive, and many people in low or moderate-income brackets who don’t receive coverage through their employers simply can’t afford the high monthly premiums. The Affordable Care Act (ACA) makes health insurance accessible to those people by providing subsidized insurance. Subsidies help reduce premiums and out-of-pocket expenses for eligible individuals and families.

ACA subsidies are health coverage tax credits that are applied toward health insurance premiums for qualified individuals. Subsidies help to keep insurance premiums affordable for people with low or moderate incomes. They work on a sliding scale based on income level and are generally adjusted proportionately to rising premiums to help insulate recipients from premium increases. In 2020, approximately 87% of the 10.7 million Americans who purchased health insurance through the marketplace received subsidies for their ACA premiums.

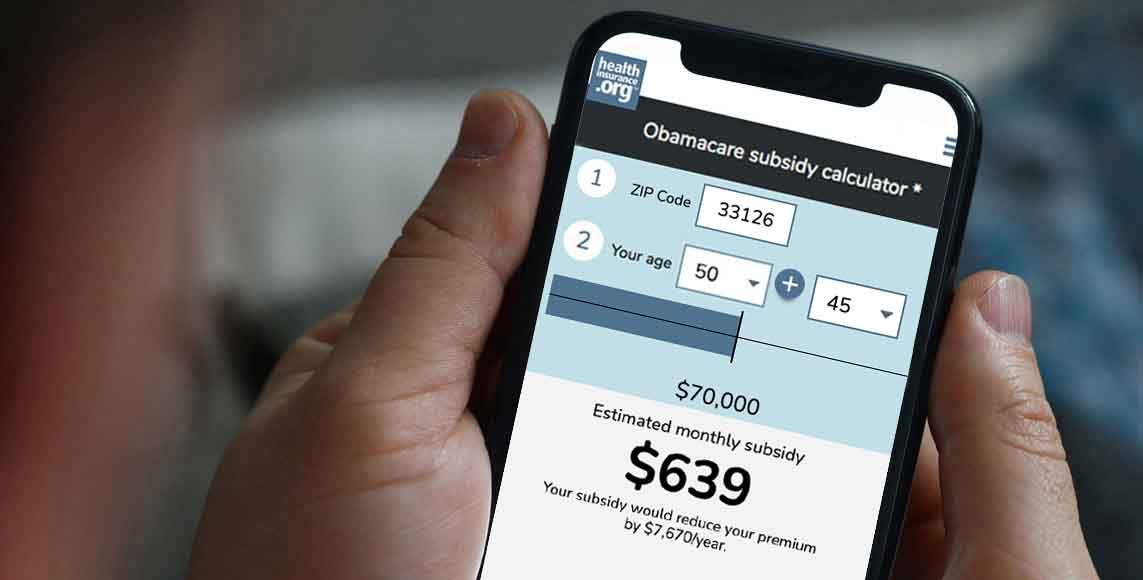

Premium credits are applied toward your monthly premium payments for plans purchased through the marketplace to reduce the cost. You have the option to have the credit paid in advance directly to the plan insurer every month or claim the credit later in a tax return. The advance premium tax credit (APTC) option pays 1/12 of the credit directly to the insurance provider every month, thereby reducing the amount you must pay. The amount of the credit is based on estimated income for the coming year. The lower the income, the higher the subsidy.

Cost-sharing credits reduce your responsibility for other out-of-pocket expenses, such as deductibles, copayments, and coinsurance. Like premium credits, cost-sharing credits work on a sliding scale based on income. Those with lower incomes will receive more generous subsidies than those with higher incomes. However, unlike premium credits, which are available for any metal level of coverage ― Bronze, Silver, Gold, or Platinum ― cost-sharing credits are only available under Silver plans to make the actuarial value more like a Gold or Platinum plan.

For example, if the annual cost of a Silver plan is $6,000 and you earn 300% of the federal poverty level (FPL) of $40,770, your required annual premium contribution for essential health services would be 6% of $40,770, or 2,446.20 (the premium tax credit would be 3,553.80).

Federal authorities have arrested Zhan Petrosyants, accusing him of running a massive no-fault auto insurance fraud ring that funneled tens of millions of dollars through fake medical claims and money laundering.

Federal authorities have arrested Zhan Petrosyants, accusing him of running a massive no-fault auto insurance fraud ring that funneled tens of millions of dollars through fake medical claims and money laundering.