China’s massive electric-vehicle insurance market is reeling, with losses mounting as insurers’ risk models struggle to keep pace with shifting vehicle economics and changing driver habits.

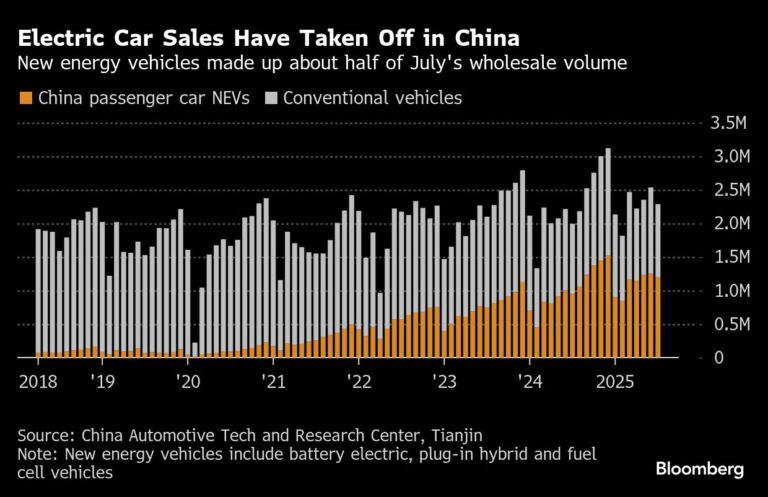

China now counts tens of millions of electric cars on its roads, with sales surging at breakneck speed. Insurers report that owners of these new-energy vehicles—who skew younger than their gasoline-car counterparts—are nearly twice as likely to file claims, and when accidents happen, the repair bills run markedly higher.

Yet even as EV drivers pay premiums 20% to nearly twice as high as those for traditional cars, China’s auto insurers have been absorbing losses on new-energy vehicle coverage for at least three years. In 2024 alone, the industry racked up 5.7 billion yuan ($802 million) in underwriting losses, according to the China Association of Actuaries—and it’s on pace to post another deficit this year.

The challenges facing Chinese insurers echo those emerging worldwide, underscoring how hard it is to price risk in even the most advanced EV market. In China, companies are now scrutinizing which policyholders may be driving for ride-hailing services—raising their accident risk—and which vehicle models carry higher inherent dangers.

EVs deliver quicker acceleration than gasoline cars, but their floor-mounted batteries are vulnerable to damage when drivers hit bumps at speed. Those complex battery systems can account for up to a third of a vehicle’s total value and rely on costly, hard-to-find components, driving repair costs sharply higher.

Some ride-hailing drivers have listed their vehicles as “private use” to secure cheaper premiums, creating a headache for insurers. Meanwhile, historical data on vehicle types and driving patterns grows obsolete fast as new models flood the market.

The upshot is that “insurers have not really managed to fully differentiate between different brands, different models, and different loss patterns, to find a way to make a profit,” said Qin Lu, CEO of Greater China at insurance broker Aon Plc.

“It’s an incredibly tough market,” Lu added, predicting that many insurers may struggle for at least another three years to stem the losses. With EVs now outselling gasoline cars, finding a fix is urgent, he said. “We are just right now in the middle of it. The industry as a whole is trying to find its way to make it work.”

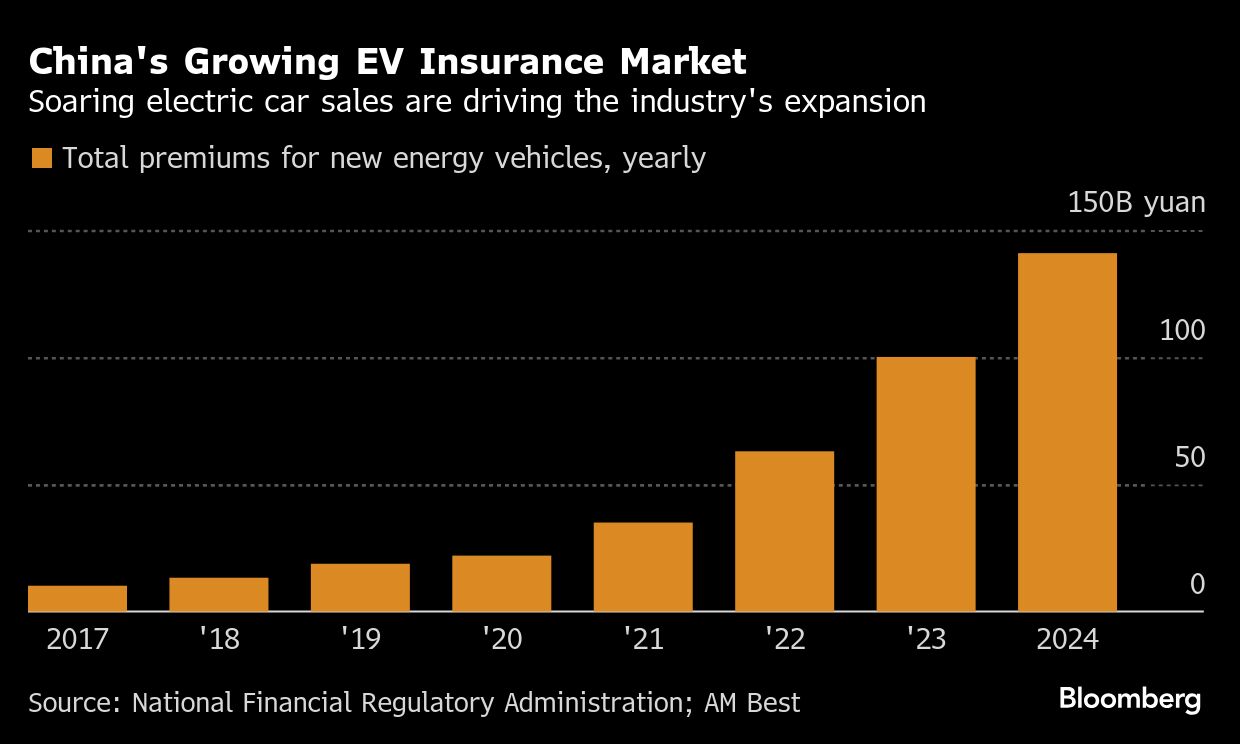

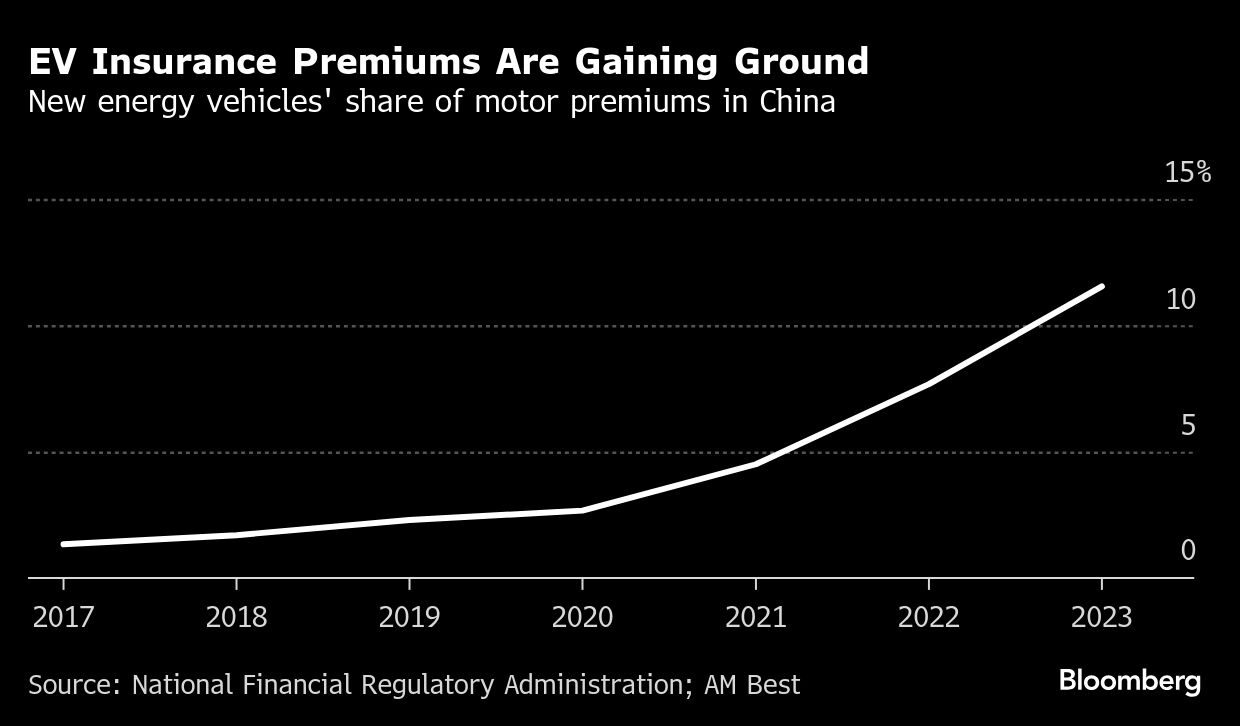

Chinese insurers collected 141 billion yuan in EV premiums last year, according to the actuaries’ association. Research from Bocom International projects that figure could soar to 500 billion yuan by 2030, when electric vehicles are expected to account for more than a third of the nation’s auto insurance market.

“EV insurance pricing is still in a trial-and-error phase,” said Wenwen Chen, an analyst at S&P Global Ratings, even as premiums for these vehicles are poised to become “the future growth engine” for auto insurers.

Higher Premiums

Nicole Wu, 38, a media professional in Hangzhou, said she purchased an imported Tesla Model 3 in 2019 and experienced several accidents that required costly repairs. In one instance, her insurer covered over 70,000 yuan in damages, partly because the car could only be serviced at an official Tesla body shop.

Over the years, her insurance premiums quadrupled, climbing to nearly 30,000 yuan a year. “It’s just horrifying!” she exclaimed. Wu ultimately chose a more affordable plan—about one-fifth the cost—that offered only the mandatory liability coverage for traffic accidents, with minimal protection for third parties. “But then it really made me anxious when I drove the car,” she recounted.

Wu said she sold her Tesla last year and switched to a more affordable electric vehicle from Nio Inc. She now pays roughly 7,000 yuan for insurance through a Nio-recommended provider, whose after-sales service can efficiently handle any repairs.

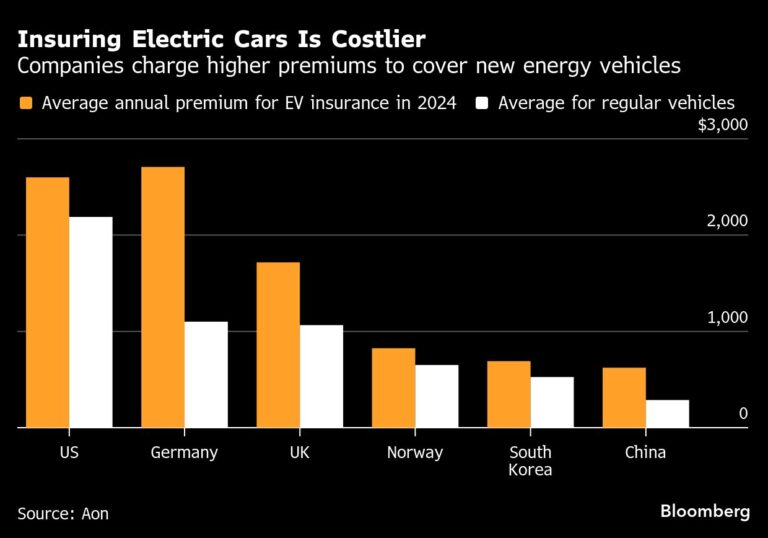

In China, the average annual EV insurance premium stands at roughly 4,487 yuan, according to Aon data—only about a quarter of what electric-vehicle owners typically pay in the United States.

New-energy vehicles in China are also far cheaper than their U.S. counterparts. In August, their average price was 158,900 yuan—around 80% of the cost of hybrid cars and 90% of traditional gasoline vehicles, according to the Autohome Research Institute, an industry analysis firm.

Over the past year, some Chinese insurers have raised premiums or pulled back from offering EV policies, leaving owners scrambling for affordable coverage. So far, these higher costs have shown little effect on overall electric-vehicle sales.

To tackle the challenge, Chinese authorities launched a platform called “Easy to Insure” in January, linking EV owners with insurance providers. The initiative has so far facilitated coverage for over 500,000 vehicles, totaling approximately 494.8 billion yuan.

“The platform doesn’t promise the lowest premiums,” said Zhang Lei, CEO of insure-tech firm Cheche Group Inc., which developed it, “but it does guarantee that applicants will not be turned away.”

Auto insurers in China do not have free rein over pricing. Regulators establish base premiums according to factors such as vehicle type and usage, while companies may adjust rates up or down within a designated range based on individual drivers’ risk profiles.

In January, Chinese regulators issued comprehensive guidelines directing companies to reduce the cost of replacement parts and repairs for new-energy vehicles and to foster “cross-industry data sharing” and collaboration. The rules also prohibit insurers from refusing customers or denying them mandatory traffic insurance.

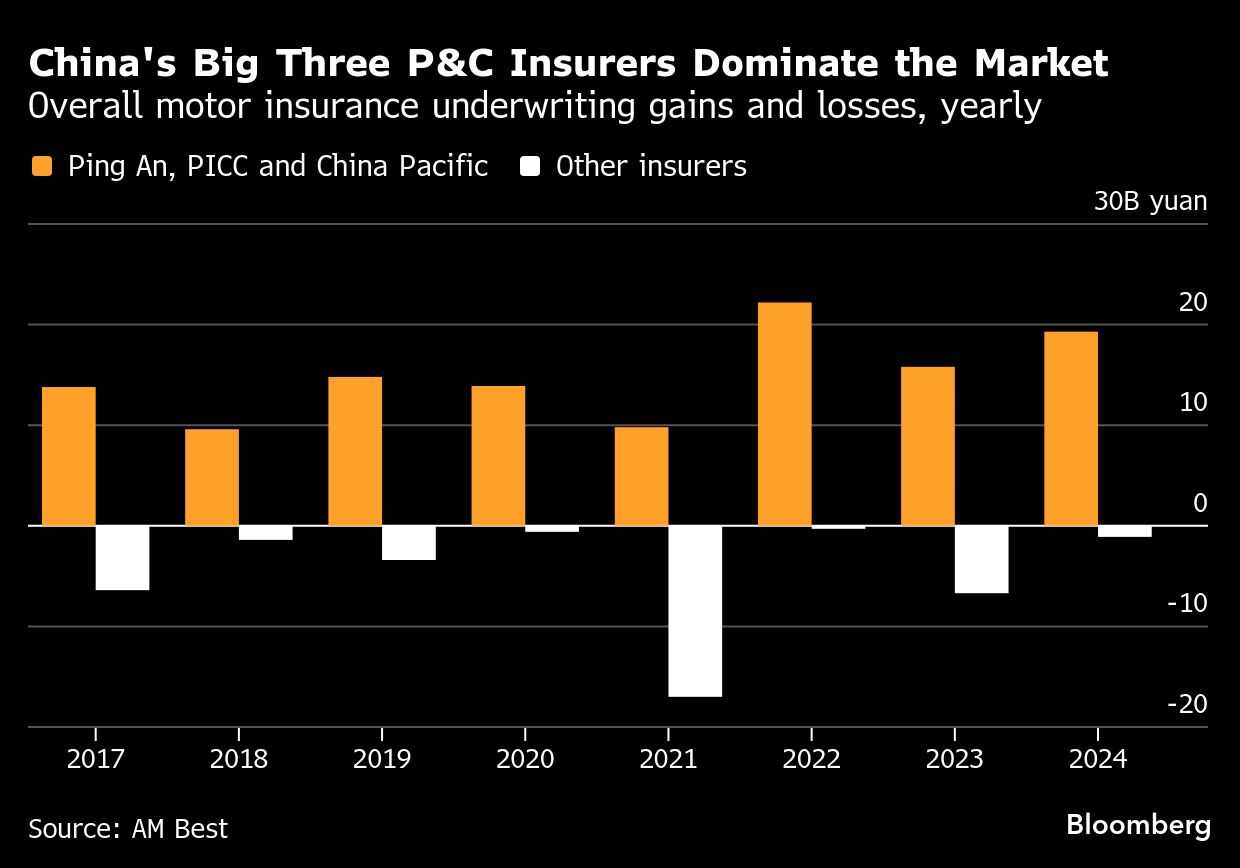

Big Three

China is home to more than 60 auto insurance companies, with the three largest firms collectively controlling at least 65% of the market, according to Aon.

Several automakers are also targeting China’s EV insurance market. Xiaomi Corp., BNP Paribas SA, and Volkswagen AG have partnered to launch a new property and casualty insurer, while Tesla—whose Chinese sales account for roughly a third of its global total—established an insurance brokerage last year. BYD Co. similarly runs its own insurance operation in the country.

According to official data, China’s insurance industry recorded an average combined ratio of 107% for new-energy vehicles in 2024, down slightly from 109% in 2023. A combined ratio above 100% indicates an underwriting loss, meaning insurers are paying out more in claims and expenses than they collect in premiums. Many smaller insurers in China have struggled to turn a profit even on traditional auto policies, hindered by limited scale and pricing power.

Ping An Property & Casualty, a division of one of China’s largest insurers, Ping An Insurance Group Co., reported underwriting profits from its EV business in 2024 and the first half of this year. The company said it has developed technology to differentiate ride-hailing drivers from other car owners and has been studying the “economics of repair” while collaborating with automakers "to identify accident scenarios and enhance vehicle design."

Ping An’s main competitors, PICC Property & Casualty Co. and China Pacific Insurance Group Co., recently reported combined ratios exceeding 100% for commercial EV insurance, indicating losses, while their underwriting of EV policies for private and household use remained profitable.

“Profit is important, but insurance companies also have social responsibilities to fulfill,” said Paul Low, CEO at the Asian Institute of Insurance. “China’s national agenda is to push for EVs and affordability is important.”

Photo: Cyclists and vehicles travel along a road in Beijing on Sept. 2, 2025; photo credit: Qilai Shen/Bloomberg