Swiss Re warns that U.S. tariff policies are undermining trade and stoking geopolitical tensions, contributing to a broader slowdown in global growth and, in turn, insurance premium expansion.

The Swiss Re Institute forecasts that global GDP growth, adjusted for inflation, will slow from 2.8% in 2024 to 2.3% in 2025, before edging slightly higher to 2.4% in 2026, as outlined in its report “World insurance in 2025: a riskier, more fragmented world order.”

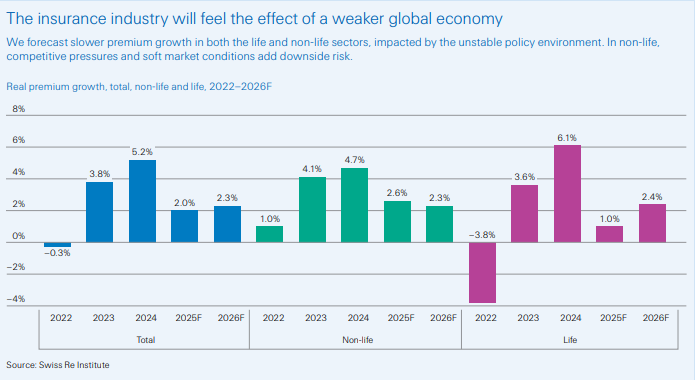

Swiss Re expects global life and non-life insurance premiums to decelerate sharply, falling from 5.2% growth in 2024 to just 2% in 2025, with only a modest rebound to 2.3% anticipated in 2026.

“U.S. tariffs create new risks for insurers, with negative impacts expected through inflation, trade, supply chain and economic growth outcomes,” the report said.

Property/Casualty Sector

“The primary non-life insurance sector is seeing decelerating premium growth as insurance pricing softens and policy uncertainty cuts economic momentum,” said Swiss Re, forecasting 2.6% growth in real terms in 2025 (versus 4.7% in 2024) and 2.3% in 2026.

Real premium growth in advanced markets rose to 4.5% in 2024, outpacing the 3.8% recorded in 2023 and the 10-year average of 3.5%, the report noted. This decade-high growth was largely driven by rate hardening, as insurers raised prices to offset escalating claims severity.

Global life insurance premium growth is projected to slow sharply, with Swiss Re forecasting a real-term increase of just 1% in 2025—down from a strong 6.1% expansion in 2024.

Localized Pricing Strength

While the impact of U.S. tariffs on the insurance industry will vary by region, Swiss Re expects the most pronounced effect to be in the United States, where rising loss trends are likely—particularly in motor and construction claims. Still, the report notes that these effects should remain manageable.

However, there will be some localized pricing strength in lines such as U.S. casualty due to higher loss cost trends, but this is unlikely “to offset the overall growth downtrend.”

Outside the U.S., Swiss Re expects tariffs to have a more disinflationary effect, which could ease pressure on insurance claims. “Premium growth will likely be lower in the environment of economic slowdown, more so in trade-exposed areas such as marine and trade credit insurance, and in sectors like construction.”

Some Opportunities

Swiss Re pointed out that, despite the challenges, the tariff crisis may open up avenues for growth in underwriting. “A heightened awareness of risk typically benefits insurers, provided that the economic shock is not severe. This is particularly the case for lines of business offering protection against economic and financial disruption, such as credit and surety insurance.”

In addition, marine insurance outside the U.S. could benefit from realignment of supply chains “if other economic blocs increase trade among themselves,” the report explained.

Investment Results to Drive Profits

Swiss Re stated that investment performance will play a crucial role in driving profitability in the property and casualty (P/C) sector over the next three years. “We see global P/C underwriting results broadly stable at around 1.5% to 2% of net premiums earned, and we estimate industry return on equity (ROE) at 9.7% from 2025 onward.”

“While insurers’ profitability outlook is still benefiting from rising investment income, we expect tariffs to slow global GDP growth, and consequently weigh on insurance demand. In the long term, US tariff policy is another move towards more market fragmentation, which would reduce the affordability and availability of insurance, and so diminish global risk resilience,” said Jérôme Haegeli, Swiss Re’s group chief economist, in a statement accompanying the report.

Stagflationary Shock

The report warned that tariff rates—at their highest levels since the Great Depression—could trigger a stagflationary shock in the U.S. economy. (Stagflation describes a situation where slow or stagnant growth, high unemployment, and rising inflation occur simultaneously.)

“The volatile nature of US policy changes under the current administration has ushered in a paradigm shift of diminished confidence in the U.S. government, eroding its status as a ‘safe haven’ for global capital,” said the reinsurer in a press release accompanying the report. “Consequently, Swiss Re Institute has lowered growth expectations for most major economies in 2025.”

Fragmentation a Danger

The terms 'fragmentation' and 'fragmented' appear 43 times throughout the report, underscoring how the fracturing of geopolitics, economies, and markets may pose significant long-term risks and costs for insurers and society alike.

“Trade barriers and supply chain disruptions or reshoring may push up inflation for prolonged periods, feeding into higher claims costs. Restrictions on free capital flows for re/insurers can lead to inefficient capital allocation, higher capital costs, and higher insurance prices, possibly curtailing insurability of peak risks,” the report added.

Swiss Re referenced the "exceptional" 2005 U.S. hurricane season, noting that 12% of U.S. insurers received reinsurance payments equal to their entire equity, while 23% received payments exceeding one-third of their equity.

(In 2005, Hurricane Katrina struck the U.S. Gulf Coast, inflicting catastrophic damage across Louisiana and Mississippi. Swiss Re described the event as a 'watershed moment' for the insurance industry in its report published on June 23, 2025. Adjusted to 2024 prices, Katrina's insured losses totaled an unprecedented $105 billion, making it the costliest natural catastrophe ever recorded for the global insurance sector, Swiss Re confirmed.)

Swiss Re cautioned in its July 9 World Insurance Report that fragmentation may impair the insurability of extreme risks, leading to limited underwriting capacity and upward pressure on insurance premiums.

“Political fragmentation reduces international cooperation on mitigating critical global risks such as climate change, pandemics, and cyber risks, increasing global exposures. Society ultimately bears the cost of fragmentation as firms and individuals have less insurance coverage, keeping protection gaps wide.”