Robust returns in the reinsurance sector are drawing in fresh capital, resulting in more favorable pricing for buyers. However, brokers’ renewal reports note that underwriting discipline remains firmly in place.

Reinsurance capacity has outstripped demand, even in the face of substantial natural catastrophe losses during the first quarter.

“[T]raditional reinsurers targeted growth and deployed more capacity at the mid-year renewals, which is accelerating the trend toward buyer-friendly conditions and leading to greater flexibility in terms and conditions as well as options to purchase expanded coverage,” said Aon in its report titled “Reinsurance Market Dynamics – Midyear 2025 Renewal.”

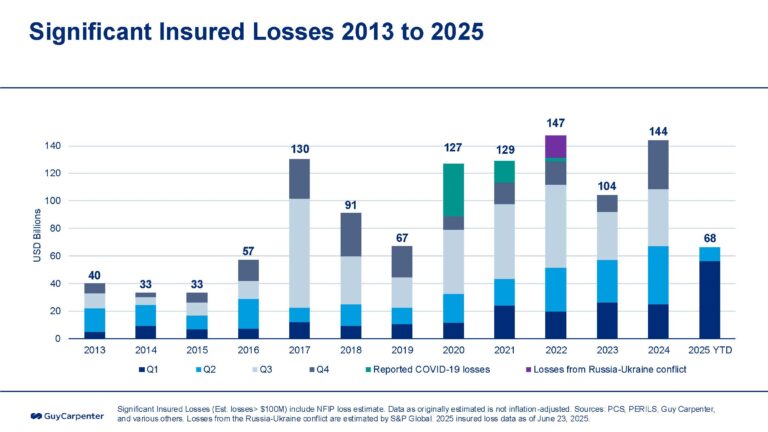

Reinsurers maintain strong balance sheets, fueling their appetite for growth even as insured losses in the first half approach $70 billion, according to Guy Carpenter’s report “Strong returns in reinsurance sector attracts capital, leading to favorable client outcomes.”

Global insured losses from natural catastrophes reached an estimated $60 billion in the first quarter alone — the second-highest Q1 total on record — largely driven by the $40 billion in losses from the California wildfires, according to Aon. “The first half of 2025 is likely to become the second costliest on record due to additional catastrophe activity in the second quarter, including two large severe weather outbreaks in the U.S. on May 14-17 and May 18-20.”

Despite this, overall pricing continued to ease at the mid-year renewals. Aon observed "significant variation in renewal outcomes," as reinsurers increasingly differentiated cedents based on their loss histories and underwriting performance.

“Clients were largely able to secure risk-adjusted rate reductions for property treaties and were well-placed to hold pricing broadly flat in casualty lines – in part, as underlying pricing increases continue to flow through to reinsurers,” agreed Gallagher Re in its report titled 1st View: Challenging the Status Quo.

“After several highly profitable years, reinsurers are increasingly looking to deploy their significant capital, but they are disciplined in approach. In some businesses and geographies, we are still seeing reinsurers willing to sacrifice share to protect profitability — particularly larger, less growth-oriented players,” said Gallagher Re.

Increasing Client Demand

Reinsurers had little difficulty meeting the 5% to 7% increase in client demand for property catastrophe limits, according to Guy Carpenter. The firm noted that reinsurer capacity exceeded demand by over 20%, resulting in risk-adjusted rate reductions of 5% to 15% for programs without recent losses, while programs affected by losses saw rate increases ranging from 10% to 20%.

“Reinsurance capacity was more than sufficient to absorb a near 10% increase in global demand for property catastrophe limit,” Aon affirmed.

Aon reported that the growing demand for reinsurance protection was primarily fueled by U.S. insurers and the substantial “depopulation” of Citizens, Florida’s windstorm insurer of last resort. In 2024, the depopulation program shifted over 428,000 Citizens policies to the private insurance market, creating additional demand for reinsurance limits among participating insurers.

“Other factors included inflation, model changes and revised views of natural catastrophe exposure, with recent wildfires in the U.S. and floods in Brazil prompting insurers to evaluate loss potential and protection needs,” Aon added.

“The number of start-up reinsurers remains small, although new players in the property catastrophe space are gaining traction and adding to competitive pressures. Competition was greatest in middle layers of catastrophe programs, in particular alternative capital created competitive tension,” Aon continued.

“The current trading environment is one of the most favorable for reinsurers in many years, evidenced by the additional capital being attracted to the sector,” said Dean Klisura, president and CEO, Guy Carpenter, in the broker’s renewal report.

“We see this as a tremendous opportunity to re-balance the market dynamics in our clients’ favor. More capacity will continue to moderate pricing, give clients more diversification of reinsurance partners, and provide better solutions to protect earnings,” Klisura added.

Casualty Renewals

Aon said casualty insurers entered the mid-year renewals in a relatively strong position “as robust underlying rating and underwriting actions taken in recent years helped ensure ongoing reinsurer support.”

“Reinsurers continue to support the casualty market, but remain watchful of negative trends in the market, including adverse reserve development, the frequency of nuclear verdicts and impact of litigation financing, as well as emerging areas of liability,” Aon added.

Gallagher Re highlighted that U.S. property/casualty insurers reported $8.1 billion in adverse prior-year development in 2024, stemming from the previous 10 accident years—more than doubling the $3.8 billion reported in 2023.

“Offsetting these concerns, however, are relatively high interest rates, the robust underlying rate environment and the underwriting actions taken by insurers in recent years,” Aon said.

Indeed, Gallagher Re highlighted the proactive measures many cedents are adopting in their underwriting strategies and claims management practices to counteract loss trends and enhance profitability.

Gallagher indicated in its report that these corrective measures taken by ceding companies have ultimately led to more favorable renewal outcomes.

“Reinsurers showed greater confidence in those cedents who articulated the actions they have taken to improve performance, and how their actions tangibly improve future performance,” Gallagher Re said.

Conversely, Gallagher noted a distinct market divide for cedents unable to demonstrate to reinsurers their efforts in addressing performance challenges. These insurers faced less favorable renewal results.

Guy Carpenter confirmed that casualty reinsurance renewals continued to reflect disciplined underwriting, with two key factors contributing to the relatively stable outcomes.

“First, reinsurers and clients evaluated trading relationships across property, casualty, and specialty programs. Reinsurers looked to find balanced support across all programs for a given client,” Guy Carpenter said. “Second, carrier underwriting actions have improved casualty economics for reinsurers, particularly proportional programs where insurers share ground-up premium and loss.”

“Reinsurers continue to be attracted to international placements with limited severity loss and good geographic diversification,” Aon added. “However, accounts with U.S. exposures that experienced further deterioration in U.S. loss severity saw a significant reduction in reinsurer appetite and increased pricing.”

Strong Reinsurer Performance

The 2025 renewals, occurring in April and mid-year, have been significantly influenced by reinsurers’ robust profits and strong capital positions.

“Reinsurers came into the renewal in good financial shape. They reported strong results for 2024, with ROEs well above the cost of capital,” said Gallagher Re. “Q1 results were weaker due to the impact of January’s unprecedented wildfires in Los Angeles, California, but barring further exception cat events, reinsurers remain on track for another good year overall.”

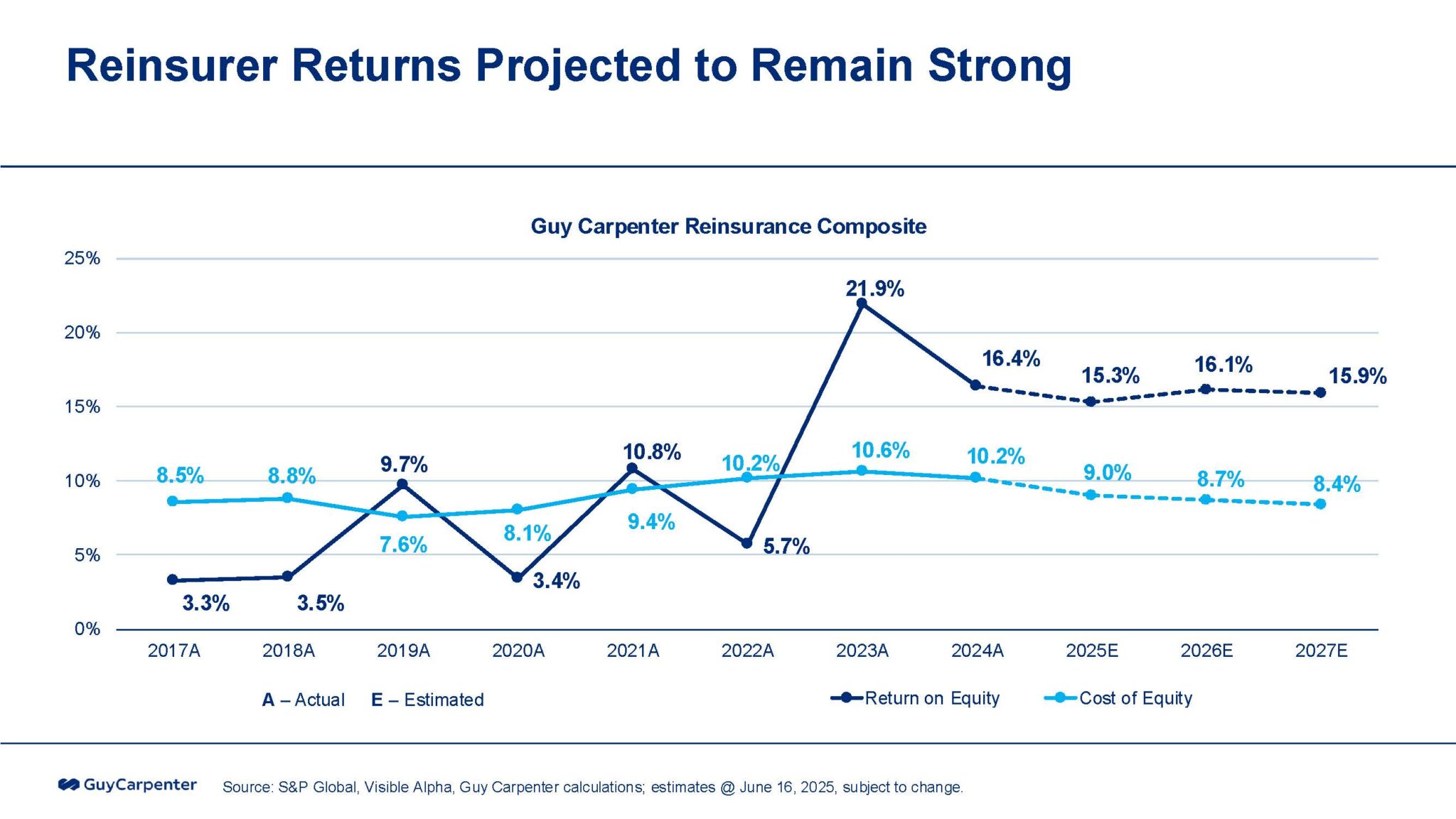

Carpenter echoed this sentiment, stating that strong reinsurer performance is anticipated to persist throughout the year, despite substantial natural catastrophe claims in the first quarter. “Reinsurer returns on equity were 16% in 2024 and are projected to be 15% in 2025,” Guy Carpenter added.

Aon reported that the majority of leading reinsurers are on track to achieve strong results in 2025. “Notably, the four composite European reinsurers have maintained their (increased) full-year earnings guidance, despite the impact of the California wildfires.”

Record Reinsurance Capital Levels

Reinsurance capital reached a record high of $607 billion at the close of 2024, with Guy Carpenter forecasting continued growth of 5% to 7% by the end of 2025.

Conversely, Aon reported that global reinsurer capital hit a new peak of $715 billion in 2024 and further increased by $5 billion to $720 billion during the first quarter of 2025, despite the impact of California wildfire claims. According to Mike Van Slooten, Head of Market Analysis at Aon, in an email explanation, the $720 billion total includes $115 billion of alternative capital.

Gallagher estimated that dedicated reinsurance capital, including alternative capital like insurance-linked securities, stood at USD 769 billion at the end of 2024 and is projected to grow by an additional 6% in 2025, assuming average performance for the rest of the year.

Aon and Gallagher Re noted that the primary catalyst for growth in reinsurance capital remains the retained earnings of established reinsurers.

“Strong capital positions are continuing to translate into healthy risk appetites, particularly in property and most specialty classes, and these dynamics are expected to persist into future renewals,” Aon added.

Insurance Linked Securities

Gallagher Re noted that capital supply has been bolstered by inflows into the insurance-linked securities (ILS) market, highlighting a $4 billion increase in non-life ILS assets under management during the first quarter. This growth supported $15.2 billion in catastrophe bond issuance through June 13, marking a 36% year-on-year rise.

Guy Carpenter confirmed that client demand for property catastrophe coverage is being well-served by a robust catastrophe bond market. “During the first half of 2025, approximately $17 billion of limit was placed through 56 property catastrophe bonds and one health catastrophe bond,” the firm stated, noting that GC Securities has placed 23 catastrophe bonds this year—the highest total among brokers to date.

Aon reported that total capacity from insurance-linked securities (ILS) surpassed $115 billion by the end of Q1 2025, driven predominantly by the expanding 144A catastrophe bond market. Additionally, Aon noted growing interest from institutional investors in sidecar opportunities, particularly within casualty risk.