ITR filing: How to calculate net annual value from house property, deductions allowed from rental income Read here to find out how is NAV calculated and which deduction can you claim if you have put your house on rent

For a landlord earning rental income, it is important to calculate the Net Annual Value (NAV) of his house. It is based on this NAV one can claim the eligible tax deductions. The value arrived at after claiming eligible deductions will be the 'income from house property' on which tax liability will be calculated.According to income tax laws, the NAV of a house property is to be calculated in two situations:

A) when house is on rent; or

B) when it is assumed to be put on rent, i.e., deemed rent

"Landlords need to select the ITR form based on their residency status (Resident or NRI), taxable income and type of income. For resident individuals having one house property, ITR 1 should be filed. In the case of other individuals, ITR 2 is applicable for income other than business or profession. Else, they are required to file ITR 3," said Neeraj Agarwala, Partner, Nangia Andersen India, a Business Advisory Company.

How to calculate NAV of a house property for income tax?

To calculate the NAV of the house property, the first step is to calculate its Gross Annual Value (GAV). You Might Also Like:

How to calculate gross annual value of house property for ITR filing

Follow the steps below to calculate the GAV.

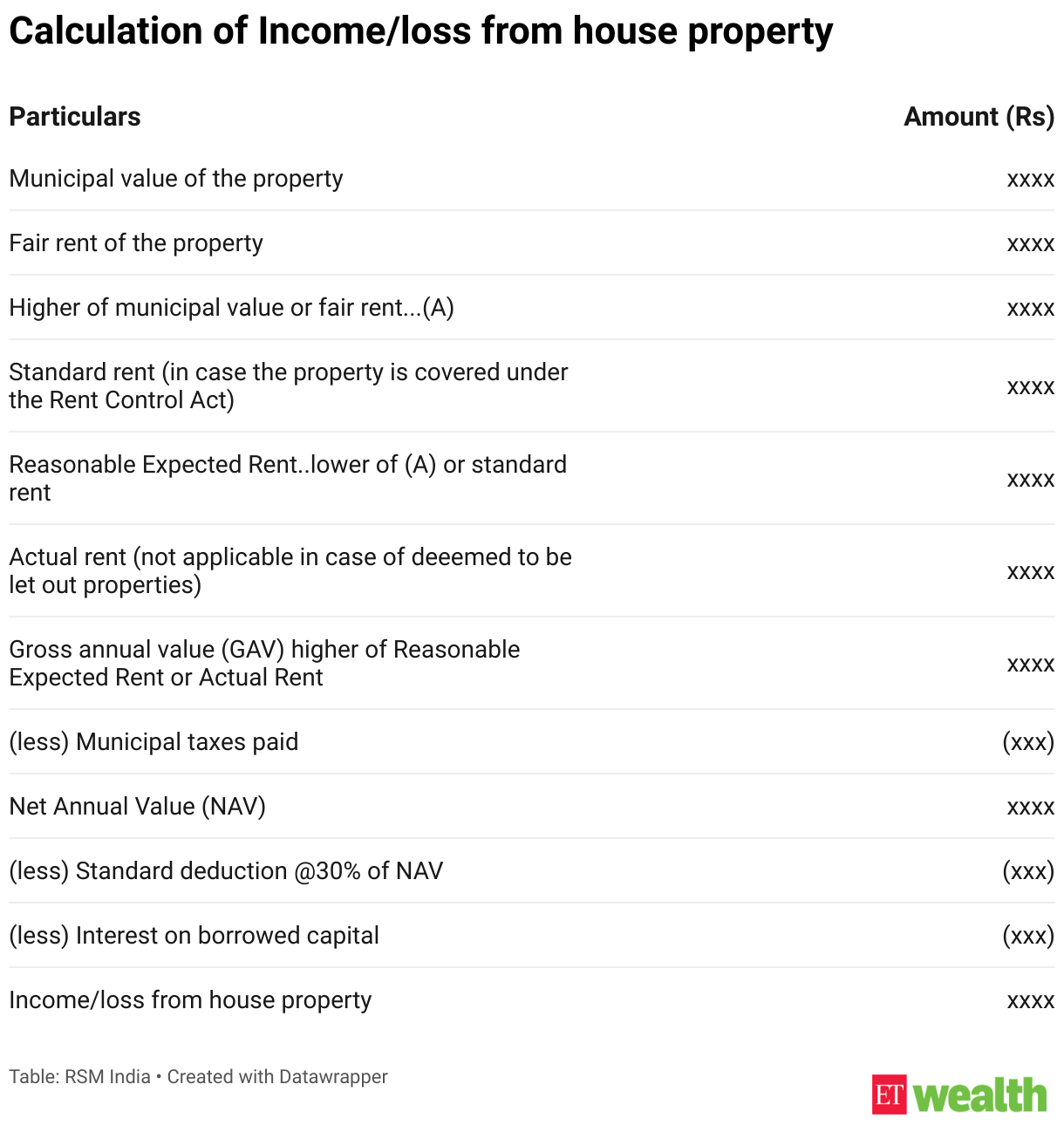

Step 1: Know the municipal rent value and fair rent value. Depending upon the area in which house is located, the municipal corporation will have a value assigned to the house based on their own calculations. This is called municipal value of the house. The fair rent value of a house is arrived at by comparing the rental value of the similar houses in the same locality. Once both the values are known, compare the municipal rent value with the fair rent, and take the higher of the two.

Step 2: Next, compare the value derived in step 1 with the standard rent (if Rent Control Act is applicable) and take the lower of the two values. This value derived from step 2 is called Reasonable Expected Rent. Do note that the expected rent cannot exceed the standard rent.

Step 3: In this step, compare the expected rent with the actual rent received and take the higher of the two values. The value arrived at here is the GAV). For deemed rent, expected rent is the GAV of the house. This is because there is no actual rent received.

Click here to read how the GAV of a self-occupied house is calculated.

From the GAV, deduct the municipal taxes or property taxes paid during the financial year, to get the NAV.

Once the NAV of the house is calculated, an individual can claim the eligible deductions to know the income from house property for ITR filing.

Deductions allowed from rental income

If the house is on rent or deemed to be on rent, then an individual is eligible for certain deductions. These are: standard deduction of 30% from NAV and interest paid on home loan, if any.The standard deduction of 30% of NAV is the umbrella deduction under which all the other house expenses like maintenance, cleaning, upkeep, etc are taken. So, no further deduction is allowed apart from this. If the house was taken on loan, then the interest paid can be claimed as a deduction from the NAV. Ask your lender to furnish you with an annual interest certificate, so that you may know exactly how much of your EMI is paid for interest and then input the correct figure in the calculation.

The final value arrived at after subtracting the eligible deductions will be 'income from house property'. This income can either be positive or negative. The value will be negative if there is a loss from house property. Now depending upon the tax regime, i.e., old or new, this loss from house property may or may not be allowed to be set-off from other sources of income such as salary, capital gains, business or profession, etc.

Click here to read what deductions and losses cannot be claimed in the new tax regime.

Key points to know about let-out house property:

Multiple houses on rent must be calculated separately: "Individuals owning multiple house properties would be required to compute the income from each house property separately and accordingly claim the necessary deductions," said Dr. Suresh Surana, Founder, RSM India, a tax, accounting and consulting company. This means that for each house standard deduction of 30% and interest on home loan deduction will be calculated separately. If opting for the new tax regime: "Under the new tax regime, if you have taken a housing loan for a property that you have rented out, you can claim the interest paid on the loan under section 24(b). However, there is a restriction on the deduction. The interest paid on the housing loan can only be deducted from the rental income to the extent that it reduces the taxable income from the house property to zero," said Saakar S Yadav, founder, and director of myITreturn.com, a tax filing assistance company.

Let us assume that the NAV of your house property is Rs 1.2 lakh and the interest paid on the home loan is Rs 1.8 lakh. In this case, you can claim the interest deduction only up to Rs 1.2 lakh. There will be a loss of Rs 60,000 under the head 'income from house property'. This loss of Rs 60,000 cannot be claimed under the new tax regime and neither can this loss be set-off or carried forward.

Municipal taxes and standard deduction are available: One can claim all the maintenance and other routine house charges under the 30% umbrella limit of standard deduction. Municipal taxes which were actually paid can also be separately claimed as a deduction for let-out houses. Do note that these deductions cannot be claimed for self-occupied property. Click here to read more about this.

Don’t miss out on ET Prime stories! Get your daily dose of business updates on WhatsApp. click here!

This story originally appeared on: India Times - Author:Faqs of Insurances